The Impact of New Individual Income Tax Laws on

Foreign Individuals Working in China

By Manuel Torres, Managing Partner of Garrigues China and Diego D’Alma, Partner of Tax Department and Cynthia Zhou, Senior Associate of Tax Department

After seeking public comments on a number of revised drafts in relation to the new individual income tax (“IIT”) laws, the following laws and regulations have come into force on January 1, 2019:

After seeking public comments on a number of revised drafts in relation to the new individual income tax (“IIT”) laws, the following laws and regulations have come into force on January 1, 2019:

- Order of the President of the People's Republic of China No.9, Individual Income Tax Law of the People’s Republic of China (revised in 2018), issued by the Standing Committee of the National People’s Congress on August 31, 2018 (“IIT Law 2018”);

- Order of the State Council of the People's Republic of China No.707, Implementing Regulations for the Individual Income Tax Law of the People’s Republic of China (revised in 2018), issued by the State Council on December 18, 2018 (“Implementing Regulations”);

- Guo Fa [2018] No.41, Circular of State Council on Issuing the Interim Measures for Additional Special Deductions for Individual Income Tax, issued by the State Council on December 13, 2018 (“Circular 41”);

- Announcement of the State Administration of Taxation (“SAT”) [2018] No.56, Announcement of the State Administration of Taxation on Transitional Matters relating to Tax Collection and Administration for Fully Enforcing the Latest Individual Income Tax Law, issued by the SAT on December 19, 2018 (“Announcement 56”);

- Announcement of the SAT [2018] No.59, Announcement of the State Administration of Taxation on Matters relating to the Taxpayer Identification Numbers of Natural Persons, issued by the SAT on December 17, 2018 (“Announcement 59”)

- Announcement of the SAT [2018] No.61, Announcement of the State Administration of Taxation on Issuing the Administrative Measures for the Withholding and Declaration of Individual Income Tax (for Trial Implementation), issued by the SAT on December 21, 2018 (“Announcement 61”); and

- Cai Shui [2018] No.164, Circular on Issues concerning the Connection of Relevant Preferential Policies after the Revision of the Law on Individual Income Tax, issued by Ministry of Finance and SAT on December 27, 2018 (“Circular 164”).

This article highlights the impact of new IIT laws on the foreign individuals working in China (excluding Hong Kong, Macau and Taiwan), based on the aforementioned laws and regulations.

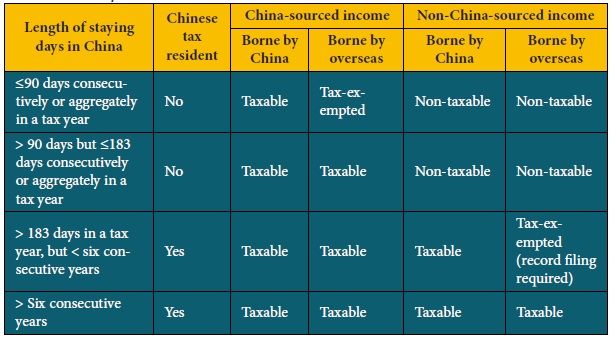

1. Distinction between Chinese tax resident and non-Chinese tax resident

1. Distinction between Chinese tax resident and non-Chinese tax resident

An individual who has a domicile in China or has no domicile in China, but has stayed in China for 183 days in aggregate in a tax year, shall be regarded as tax resident.

On the other hand, an individual, who has no domicile (“Non-domiciled Individuals”) in China and has stayed in China for less than 183 days in aggregate in a tax year, shall be regarded as non-tax resident.

2. IIT liabilities of Non-domiciled individuals

In principal, the tax resident shall pay IIT on income derived from China and overseas, whereas the non-tax resident shall pay IIT on income derived from China.

Under the Implementing Regulations, Non-domiciled Individuals could be exempted from overseas sourced income not borne by Chinese entities, other economic organizations or individuals, provided that the tax years (i.e. January 1 to December 31) in which the individuals stay in China for more than 183 days do not exceed 6 consecutive years and the relevant record filing has been performed with the competent tax authority. If the individual has a single trip exceeding 30 days during any tax year in which he stays for more than 183 days, the count of the consecutive years with more than 183 days in China shall restart again.

Non-domiciled Individual, who has resided in China for an aggregate period of no more than 90 days in a tax year, may be exempted from IIT for the income that is sourced from China, but is paid by an employer outside the territory of China and is not borne by any organization or office of the relevant employer located in China.

The IIT liability of Non-domiciled Individual is summarized in the table below:

It is worth mentioning that the IIT Law 2018 has shortened the time period of being qualified as a tax resident in China from one year to 183 days in a tax year. Such change may result in foreign individuals working in China being more likely to become tax residents in China. Although the Implementing Regulations has extended the previous five-year rule to the six-year rule for the taxation of worldwide income on the Non-domiciled Individuals, the 90 days consecutively or aggregately in a tax year to break the count of consecutive years are removed. Only a single trip exceeding 30 days during a tax year in which the individual stays for more than 183 days may break the count of the consecutive years.

It is worth mentioning that the IIT Law 2018 has shortened the time period of being qualified as a tax resident in China from one year to 183 days in a tax year. Such change may result in foreign individuals working in China being more likely to become tax residents in China. Although the Implementing Regulations has extended the previous five-year rule to the six-year rule for the taxation of worldwide income on the Non-domiciled Individuals, the 90 days consecutively or aggregately in a tax year to break the count of consecutive years are removed. Only a single trip exceeding 30 days during a tax year in which the individual stays for more than 183 days may break the count of the consecutive years.

3. Additional special deductions vs. IIT exempted benefits in kind

The IIT Law 2018 newly introduces a number of additional special deduction items on comprehensive income for tax residents (“Additional Special Deduction Items”), including children’s education expenses, continuing education expenses, medical expenses for serious diseases, interest for housing loan, rental expenses and care for elderly.

Circular 41 has further clarified the conditions to apply the additional special deductions, the eligible period of time, the standard limit of deductions, the reporting and documentation requirement, etc.

Nevertheless, foreign individuals, who are qualified as Chinese tax residents, may select to apply Circular 41 or the preferential IIT-exempted policies on allowances in accordance with Cai Shui Zi [1994] No.20 , Guo Shui Fa [1997] No. 54 and Cai Shui [2004] No.29 (collectively referred to as “IIT-exempted Policies”). After making such choice, foreign individuals cannot make changes within a tax year. Nevertheless, the IIT-exempted Policies will be invalid from January 1, 2022.

In comparison between Circular 41 and the IIT-exempted Policies, some of the Additional Special Deduction Items are usually not applicable to foreign individuals. For example, the medical expenses for serious diseases require the treatments in public hospitals. Foreign individuals usually go to private hospitals under the commercial health insurance provided by the employer. Regarding the interest for housing loan, it is rare that a foreign individual purchases a house or an apartment in China. Many foreign individuals working in China rent a house or an apartment.

Moreover, the IIT exempted amount of children’s education expenses and rental expenses under Circular 41 are relatively low. The said two expenses may be subject to much higher thresholds on a reasonable basis by obtaining the invoices from the landlord under Guo Shui Fa [1997] No. 54.

Furthermore, IIT-exempted Policies offers IIT exemption on flight tickets, relocation expenses, meal allowances and laundry expenses to foreign individuals, which are not included in the Circular 41. Most importantly, both tax residents and non-tax residents may apply IIT-exempted Policies.

Foreign individuals are suggested to review the remuneration package and consider the conditions required under each regulation for IIT exemption, so as to make a decision on which regulation to apply.

4. Different IIT computation for Chinese tax residents and non-Chinese tax residents

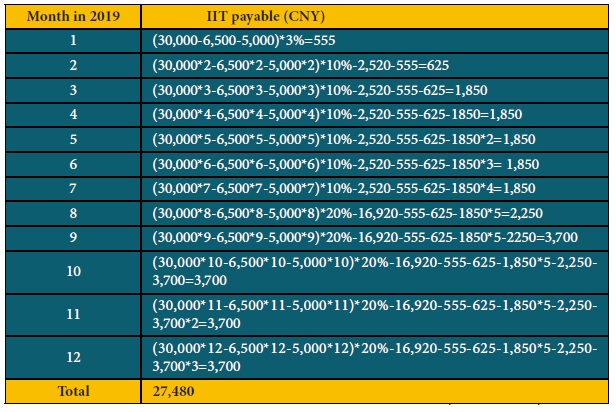

The statutory deduction for tax residents has been increased from CNY 4,800 per month on salary income (i.e. 57,600 per annum) to CNY 60,000 per annum on comprehensive income. An annual basis computation of IIT would result in a lower IIT burden in the earlier months of the year, but a higher IIT burden in the subsequent months of the year. Consequently, an individual may receive decreasing net salary over the year, assuming that the monthly gross salary remains unchanged.

For example, a foreign individual is a Chinese tax resident in 2019, who has monthly China-sourced salary income of CNY 30,000 (including meal allowances) and meal allowances of CNY 6,500 per month. The statutory personal allowance for taxable income is CNY 5,000.

The statutory deduction for non-tax residents has been increased from CNY 4,800 per month to CNY 5,000 per month on salary income. The computation of non-tax residents remains on a monthly basis, which is the same computation method before the new IIT laws. In other words, an individual may receive the same amount of net salary over the year, assuming that the monthly gross salary remains unchanged.

The statutory deduction for non-tax residents has been increased from CNY 4,800 per month to CNY 5,000 per month on salary income. The computation of non-tax residents remains on a monthly basis, which is the same computation method before the new IIT laws. In other words, an individual may receive the same amount of net salary over the year, assuming that the monthly gross salary remains unchanged.

For example, a foreign individual is a non-Chinese tax resident in 2019, who has monthly China-sourced salary income of CNY 30,000 (including meal allowances) and meal allowances of CNY 6,500 per month. The statutory personal allowance for taxable income is CNY 5,000.

5. Special tax treatment on annual bonus

5. Special tax treatment on annual bonus

According to Circular 164, the special preferential tax treatment can continue to be applied on one-off annual bonus obtained by tax resident who meets the provisions in Guo Shui Fa [2005] No.9 until December 31, 2021. The one-off annual bonus is excluded from the comprehensive income and may be divided by 12 and apply the corresponding tax rate and quick deduction listed in the Comprehensive Income Tax Rate Table converted to the monthly basis. However, the one-off annual bonus shall be included in comprehensive income in the calculation of tax payable from January 1, 2022.

It is noticed that Circular 164 has not mentioned the preferential tax treatment of one-off annual bonus for non-tax residents. In this regard, non-Chinese tax residents are not eligible for the tax preferential policy of annual bonus from January 1, 2019. Since the IIT filings are based on cash basis in China, the IIT liability of annual bonus for non-Chinese tax residents shall arise in the month in which the annual bonus is paid. Consequently, the annual bonus shall be treated as part of the monthly salary and computed together with the basic salary and allowances.

In practice, many non-tax residents have experienced the issue of not being allowed to file as a tax resident in the beginning of 2019. The tax authorities claim that the foreign individuals are not tax residents until they have satisfied the 183-day requirement. In such case, the taxation on annual bonus of foreign individuals has become a controversial issue.

Article 9 of Announcement 61 stipulates that the tax filing method of the non-Chinese tax residents may not be changed in the year of filing. In the case that a non-Chinese tax resident qualifies as a tax resident in the second half of 2019, the expatriates shall continue to file as non-tax residents. Consequently, no tax preferential policy may be applied when the bonus is received by and taxed on the foreign individual who is a non-tax resident in the beginning of 2019. A tax refund for the paid IIT on annual bonus may be performed during the annual IIT filing for the reclassification of tax resident.

6. Special tax treatment on share incentives

6. Special tax treatment on share incentives

The special preferential tax treatment may be applied to certain share incentives. According to Circular 164, under certain circumstances, IIT on stock options, stock appreciation rights, restricted shares and other share incentives (collectively referred to as “Share Incentives”) received by tax residents before December 31, 2021, can be calculated separately from comprehensive income. The full amount of Share Incentives may apply the corresponding tax rate and quick deduction in the Comprehensive Income Tax Rate Table for IIT computation. The tax preferential policy on Share Incentives after January 1, 2022, would be stipulated in the future.

7. Special tax treatment on severance payment

The special preferential tax treatment on severance payment can continue to be applied under the new IIT regulations (Article 5 of Circular 164). The one-off severance payment received from the employer (including the economic compensation, living subsidies, and other subsidies) within 3 times of the local average salary of last year can be exempted from IIT. The excess shall be calculated separately from the comprehensive income and apply tax rates and quick deductions in the Comprehensive Income Tax Rate Table.

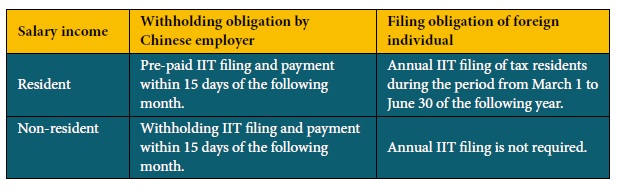

8. IIT withholding and filing obligation

The entity or individual that pays the taxable income to an individual shall be the withholding agent of the individual. Different withholding or filing obligation may arise subject to the type of income received by the individual. The below table illustrates the IIT withholding and filing obligation for salary income.

In addition to the above, there are a number of situations that may require the taxpayer to file and pay the IIT with the competent tax authorities by themselves:

In addition to the above, there are a number of situations that may require the taxpayer to file and pay the IIT with the competent tax authorities by themselves:

- Non-residents, who have derived salary income from two or more employers in China, shall file IIT on a monthly basis by themselves with the competent tax authorities respectively within 15 days of the following month in which the income is received;

- In case that the withholding agent fails to perform the withholding liability, the taxpayer shall file and pay the IIT to the competent tax authority by June 30 of the following year, unless the taxpayer is noticed by the tax authority on an earlier date of payment;

- Taxpayers that do not have a withholding agent shall file and pay the IIT to the competent tax authority within 15 day of the following month;

- Resident individual, who derives overseas sourced income, shall file and pay the IIT to the competent tax authority for the period from March 1 to June 30 of the following year.

9. Enhanced communication and transparency in information exchange.

Chinese government authorities shall provide assistance in identifying the tax identification number, tax residence status, financial account information and the information related to the Additional Special Deduction Items to the Chinese tax authorities.

Following the implementation of information exchange on financial accounts between China and other participated countries or jurisdictions by Chinese tax authorities, the first information exchange on individual accounts of non-residents with high net worth is carried out by Chinese tax authorities in September 2018, Chinese tax authorities would receive the exchanged information of Chinese tax residents from other participated countries or jurisdictions. The increasing transparency in the tax administration system may result in higher tax risks for Chinese tax residents, who have any potential tax non-compliance.

10. IIT deductible overseas sourced income

In principal, the overseas IIT paid on the overseas sourced income of a Chinese tax resident may offset against the IIT payables in China, but the offset amount shall not exceed the IIT payables as computed pursuant to the provisions of IIT Law 2018 for the taxpayer's income derived from outside China. Nevertheless, such rule has not implemented in China in the past decades. The IIT Law 2018 has addressed the issue, which is anticipated that the said law would be implemented effectively from now on.

Garrigues’ comments

Overall, the new IIT laws and regulations have tightened a number of policies to foreign individuals working in China, from the shortened period of being classified as a non-tax resident, restricted period of the validity of IIT-exempted Policies, removed tax preferential treatment of annual bonus for non-residents and the closer monitoring of worldwide income of foreign individuals.

There are still many puzzles to be clarified during the implementation of the new IIT laws and regulations, such as the reasonableness of the annual bonus treatment for foreign individuals, who are Chinese tax residents. It is also noticed that different tax authorities have different interpretations to the new IIT laws and regulations, which are expected to be unified by the SAT on an ongoing basis. Chinese companies, as the withholding agent of the foreign individuals, are recommended to discuss any question or doubt with the competent tax authorities, rather than taken-for-granted in the words of tax authorities. Both the tax authorities and the taxpayers (or the withholding agent) are considered as in the learning phase of the new IIT laws and regulations. The competent tax authorities may raise the uncertain issues to its upper level tax authority for further clarification.