Investors have soured on many Chinese companies on fears of a slowing economy and worries about accounting fraud and corporate governance. But for analysts at investment firms, the stocks remain a hot ticket.

In bullishness reminiscent of the technology bubble of the 1990s, analysts who work for investment banks based around the world rate nearly every Chinese stock they cover as a "buy." While these analysts generally are a bullish lot, they are far more positive on Chinese banks, tech companies, retailers and the like than they are on companies based elsewhere.

According to data compiled by independent research firm Forensic Asia Ltd., analysts have 19.2 "buy" recommendations on Chinese stocks for every one "sell" recommendation. For stocks of companies based in the U.S., the ratio is 10.5, and for the rest of the Asian-Pacific region it is 7.3.

"At sell-side firms, there is overwhelming pressure to believe in the 'China cannot fail' story," said Gillem Tulloch, Forensic Asia's founder and managing director and a former analyst at brokerage firm CLSA. Current and former sell-side analysts said other reasons for bullishness include obtaining better access to companies and their executives and a desire to get investment-banking and trading business from companies. Forensic Asia, which doesn't do any corporate-finance business or investing, issues slightly more "sell" than "buy" ratings in general, Mr. Tulloch said.

Investors who followed analysts' bullish recommendations haven't fared well this year. The Shanghai Composite Index has dropped 15%, and in Hong Kong, where Chinese companies account for two-thirds of the trading volume, the Hang Seng Index has fallen 23%.

The selloff in Chinese shares has come amid questions from some ratings firms, hedge funds and short sellers about corporate governance and accounting at some companies.

Last Monday, claims by short-seller Muddy Waters Research LLC against Chinese advertising company Focus Media Holding Ltd. sent the company's shares down 39% on the Nasdaq Stock Market. Analysts still have 11 buy ratings and no sell ratings on the stock. A short seller bets that a stock price will fall. Focus Media disputed Muddy Waters's claims, saying the short seller's report misinterpreted LCD-display numbers and financial data. The shares gained back about 14% by the end of the week.

Questions also have swirled around Sino-Forest Corp. This month, a special board committee said it found no fraud at the company in response to a Muddy Waters report this year that said the forestry firm misrepresented the value of its timber holdings.

An analyst who covers Asian stocks for a major bank said that, in his experience, when analysts suspect wrongdoing at a company they will drop coverage rather than issue a negative report.

"The best you can do is to suggest certain dealings are 'questionable.' Readers of our reports understand these subtleties," the analyst said.

Overly bullish analysts and conflicts of interest have been a problem in the securities industry. In the wake of the tech-stock bubble in the U.S. early last decade, Wall Street's largest securities firms agreed to pay $1.4 billion to settle government charges they issued overly optimistic investment research to curry favor with corporate clients and win investment-banking business. The settlement also included a provision that securities firms erect a firewall separating analysts from investment-banking operations. At the height, analysts' buy ratings outnumbered sell ratings by 100 to 1.

In an interview on his last day in office as Hong Kong's securities regulator this year, Martin Wheatley warned about the craze for shares of Chinese companies, calling China "the new dot-com" of the investment world.

As with the tech bubble, the rationale behind the bullishness is growth.

"For years there has been a 'who cares' attitude toward Asian company fundamentals due to high growth rates in the region," said Richard Leggett, a former Goldman Sachs Group executive who has run two independent research firms.

China's big state-controlled banks were among the largest initial public offerings in the world when they listed in recent years, but their recent stock performance has been weak, as investors worry that they are carrying bad debts on their books. On average, the big-four Chinese banks are down 29% this year in Hong Kong trading, yet analysts have remained steadfastly bullish.

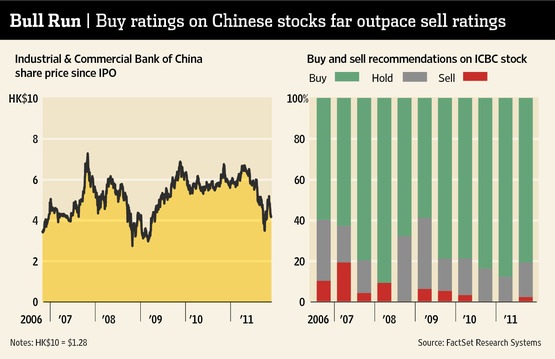

Industrial & Commercial Bank of China Ltd., the world's largest lender by market value, has 24 buy ratings and only one sell, according to FactSet Research Systems Inc. In September 2007, as banking stocks were approaching peaks, there also was only one sell rating on the lender. China Construction Bank Corp. has 25 buy ratings and one sell, according to FactSet. In 2007, there were 17 buy ratings and no sell ratings.

South Korea, where the ratio of buy to sell ratings is 22.7, is the only market where analysts are as bullish as they are in China, according to Forensic Asia. Several analysts said some Korean companies put pressure on analysts to produce positive ratings.

James Antos, a banking analyst for Mizuho Securities Co., is one of the few bears on Chinese banks, with sell ratings on six of the nine Chinese lenders he covers and no buy ratings. Mr. Antos, a former Ernst & Young auditor who has been following banks since the 1980s, blamed the bullishness on the inexperience of many analysts in Asia.

"In Europe, some guys have been covering banks for 20 years. There's a depth of understanding among Europeans and to some extent U.S. analysts that's just not here in Asia," he said. "It wouldn't be a bad thing to have at least lived through one economic cycle before you start telling people to buy bank stocks in a bear market."