Are China's surging housing prices sustainable?

By Chelsea Cai, Head of Research at JLL Tianjin

Residential market in China has witnessed skyrocketing prices over the past decade. Thanks to the easing mortgage policy and fewer restrictions in 2016, the overheated markets were not only limited to Beijing, Shanghai and Shenzhen but also spread rapidly to Tier II cities such as Tianjin, Nanjing and Hangzhou. These cities, which have rapidly growing GDPs and strong investments in infrastructure, are expected to see their economies continue to grow at above the China average for at least the next few years. After seeing property prices rise rapidly, these major Chinese cities have recently rolled out new measures to cool both the residential property and land markets. In this article, we look specifically at China's coastal city of Tianjin as an example to analyse whether the housing frenzy will be sustainable in future.

Residential market in China has witnessed skyrocketing prices over the past decade. Thanks to the easing mortgage policy and fewer restrictions in 2016, the overheated markets were not only limited to Beijing, Shanghai and Shenzhen but also spread rapidly to Tier II cities such as Tianjin, Nanjing and Hangzhou. These cities, which have rapidly growing GDPs and strong investments in infrastructure, are expected to see their economies continue to grow at above the China average for at least the next few years. After seeing property prices rise rapidly, these major Chinese cities have recently rolled out new measures to cool both the residential property and land markets. In this article, we look specifically at China's coastal city of Tianjin as an example to analyse whether the housing frenzy will be sustainable in future.

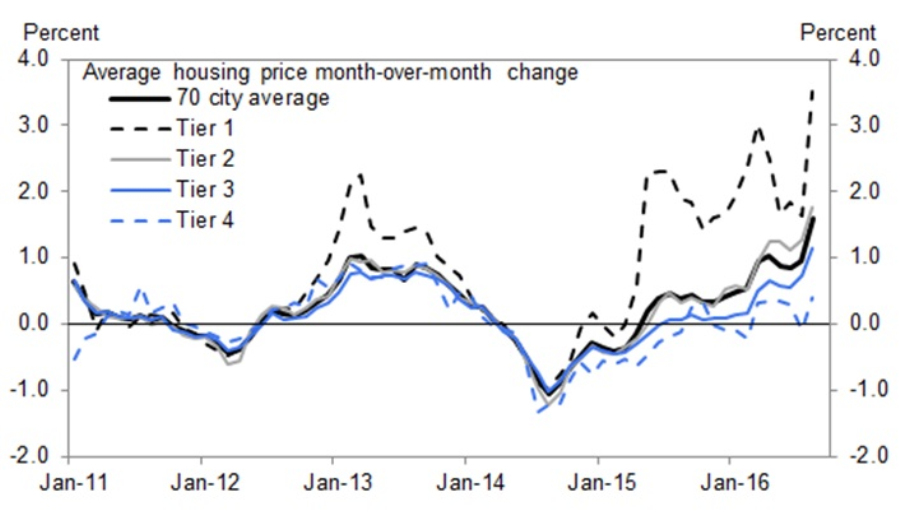

Chart 1: China 70 Cities Housing Price

Source: NBS, Zerohedge.com, Goldman Sachs

Source: NBS, Zerohedge.com, Goldman Sachs

The accompanying chart 1 shows the change in average property price (month-on-month) of newly built commodity housing amongst 70 major cities tracked by the National Bureau of Statistics. Monthly growth of China 70 cities ranges between -1.0% to 4.0% month-on-month. Tier 1 cities witnessed larger changes and Tier 2 or 3 cities followed the same pattern but were a little weaker than their Tier 1 counterparts.

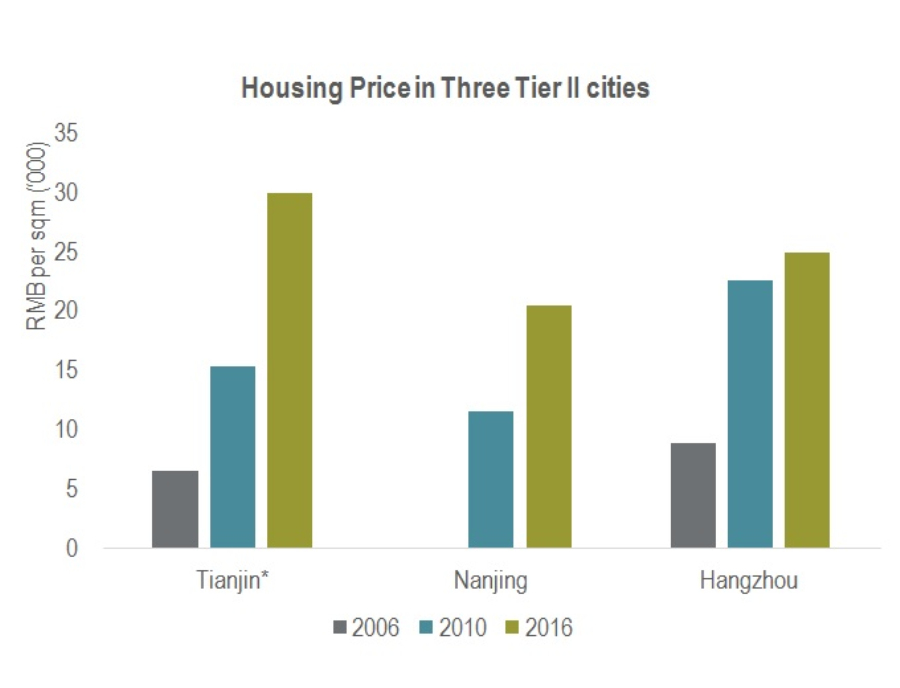

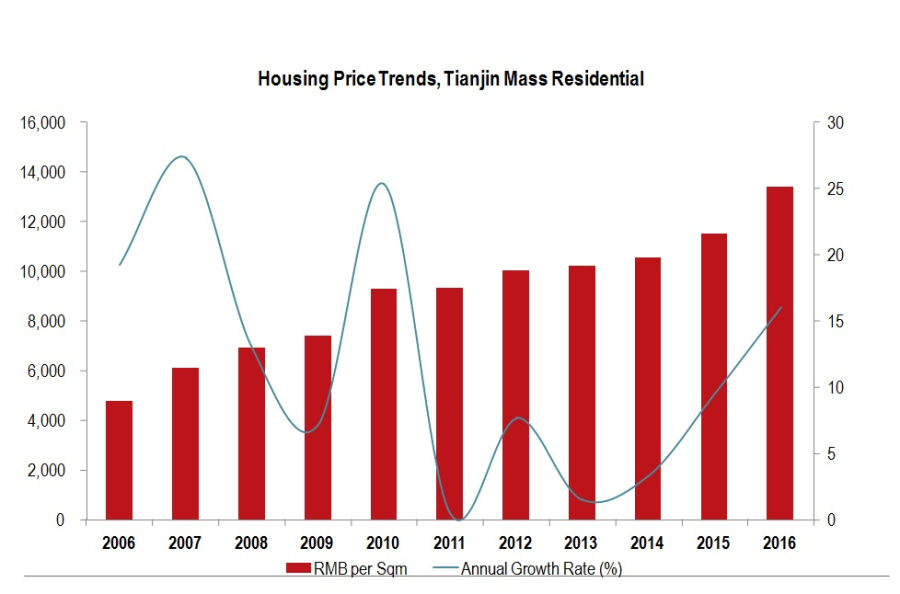

Chart 2: Housing Price in Tianjin

Source: CREIS, Tianjin Statistics Bureau, JLL Research

Source: CREIS, Tianjin Statistics Bureau, JLL Research

Residential prices in cities such as Tianjin, Nanjing and Hangzhou were strong, nearly tripling from 2006 to 2016, according to CREIS, a Chinese residential data provider.

What is pushing residential prices higher?

There are five reasons to explain the dramatic strength of housing market: economic growth, urbanisation, limited alternative investment opportunities, credit growth and land control. First, rapid economic growth in the past decade has allowed the rise of Chinese middle class and allowed them to invest heavily in the property market. Second, urbanisation resulted in a considerable portion of the population moving to major cities. Tianjin's population increased 1.5 times to 14 million from 9 million over the last ten years. This huge increase in urban population has resulted in many migrants wishing to settle down in major cities and this boosted the strong demand for residential needs.

Third, as China offers very limited investment channels to individual investors domestically, property investments are regarded as a safe and often guaranteed return, because for the last two decades this has always been the result. Different from previous years, in 2016, homebuyers largely took advantage of credit. Easier access to credit led both homebuyers and speculators to rush into the property market in the country's major cities. Last, local governments control the land market. For investing in social welfare, infrastructure, education and other public resources, local governments rely on real estate investment, particularly land sales, to generate considerable revenue. In years when they release less land to the market, prices of land and property increase. All of these reasons explain the surging housing prices for the past decade, which eventually reached new heights in 2016.

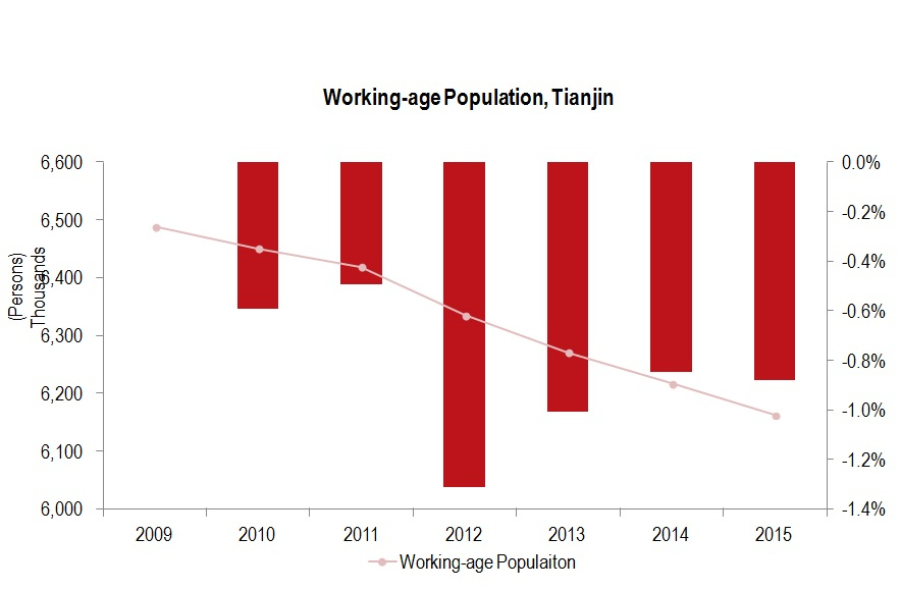

Chart 3: Working-age Population, Tianjin

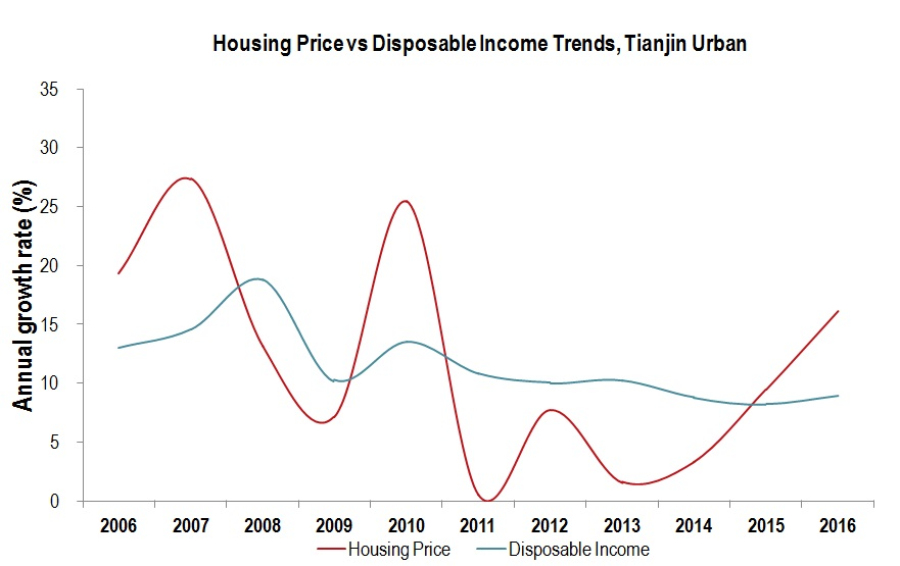

Chart 4: Housing Price vs Disposable Income, Tianjin

Chart 4: Housing Price vs Disposable Income, Tianjin

Source: CREIS, Tianjin Statistics Bureau, JLL Research

Source: CREIS, Tianjin Statistics Bureau, JLL Research

Why might the residential property market slow?

China's economy is undergoing a transformation and entering a "new normal phase" with decelerating growth rates. According to Oxford Economics data, China's annual GDP growth rate will decline to 6.0% in five years from 2016 to 2020. This will result in a slower pace of economic growth in future and will slow the pace of wealth created for the average Chinese consumer. In addition, the working-age population has been declining for the past five years (Chart 3). Retiring workers may cash out by selling houses or workers supporting retired parents may have less money to invest in the real estate market. Specifically for Tianjin, the data shows that disposable income is growing at a slower pace than real estate prices (Chart 4). This widening gap between the growth of housing prices and income will likely cause housing to become less affordable in future.

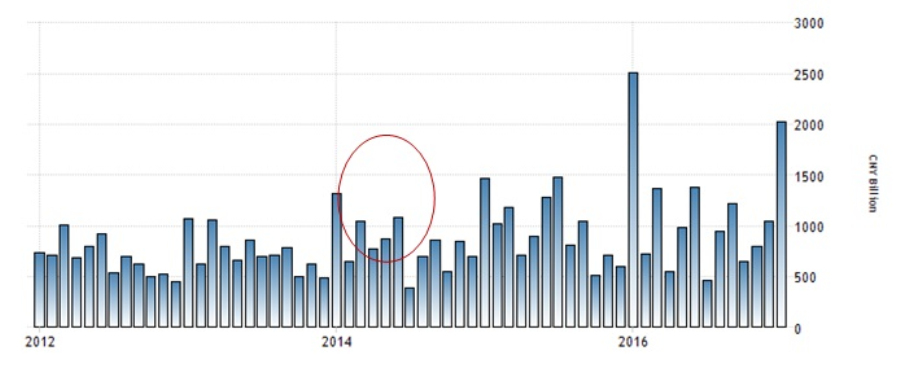

Chart 5: China New Yuan Loans

Source: PBOC, TradingEconomics.com

Source: PBOC, TradingEconomics.com

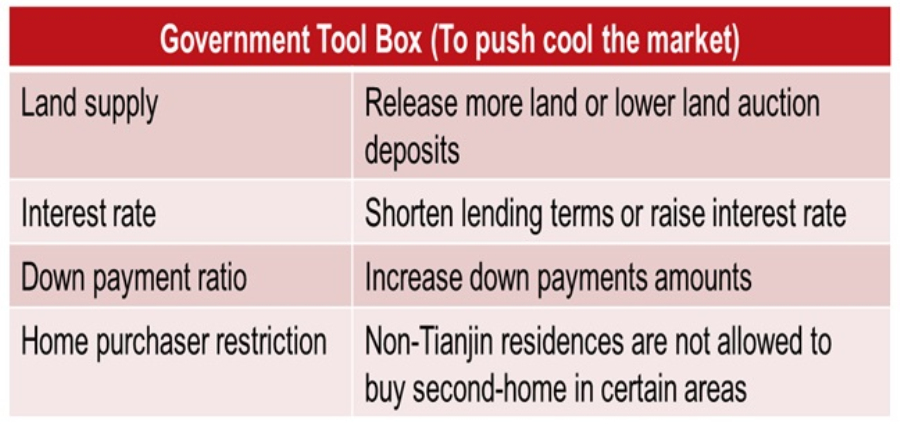

As mentioned previously, credit growth is one reason for the boost in housing demand last year. The accompanying charts show China's monthly new loan amounts increased annually and for some single months in 2016, more than 80% of new loans were for home mortgages, according to data from the People's Bank of China (Chart 5). However, Beijing is aware of the huge risk and tightening of credit growth policies is regarded as an effective way to dampen house price acceleration. Since late September, more than 20 cities have imposed rules on home purchases, with banks tightening loans to both developers and individual buyers. Following on from the policies of Beijing and other cities, Tianjin has lowered the discount on home mortgage rates (increasing borrowing rates), and banks require a strict loan screening process. By the end of 2016, Tianjin had increased down payments from 20% to 40%. These measures have cooled sales volumes and they will cause housing prices to be stable in 2017.

Moreover, as China's investment market will eventually open, Chinese people are expected to welcome investment opportunities that can diversify their portfolios, instead of putting all of their savings into the housing market. Overseas property, REITs and mutual funds will be possible new alternative investment channels for individual investors in future. In addition, there are two uncertainties that may influence the overheated property market. One is that the local governments could change their revenue sources and rely less on the land market for income, and as a result they would do less to boost land prices. Another possible uncertainty is whether the launch of a property holding tax will result in high cost for individuals to maintain property, thus reducing capital gains for speculators. We think the tax which nearly all developed countries have will eventually happen although it may be more than a decade or so away.

Conclusion

In summary, the slowing economic growth in China, decreasing working-age population, disposable income growth that is slower than the current growth in housing prices and increasing burden of retired parties will not allow Chinese to keep spending money on buying more properties. Also different government tools including tightening credit policies will help cool the demand from homebuyers. China will eventually open investment channels to diversify the choice for Chinese investors. Thereafter rapidly rising housing prices are unlikely to be sustainable over the long term.

---END---