Will a US Market Crash Bring Down China?

By Anthony

In this space last month, the emerging market fund by MSCI referred to as iShares Emerging Market ETF (EEM) was extrapolated upon regarding the inclusion of Chinese A shares or large companies within China that were previously barred from being invested in, at least directly, by foreign investors. Since the inclusion of these shares, the fund has found itself in significant positive territory rising around 5% or ballooning from about $41.14 a share to $43.70 a share. Of course though, this cannot entirely be attributed to Chinese A-shares since a number of significant Chinese stocks have been down as of late.

In this space last month, the emerging market fund by MSCI referred to as iShares Emerging Market ETF (EEM) was extrapolated upon regarding the inclusion of Chinese A shares or large companies within China that were previously barred from being invested in, at least directly, by foreign investors. Since the inclusion of these shares, the fund has found itself in significant positive territory rising around 5% or ballooning from about $41.14 a share to $43.70 a share. Of course though, this cannot entirely be attributed to Chinese A-shares since a number of significant Chinese stocks have been down as of late.

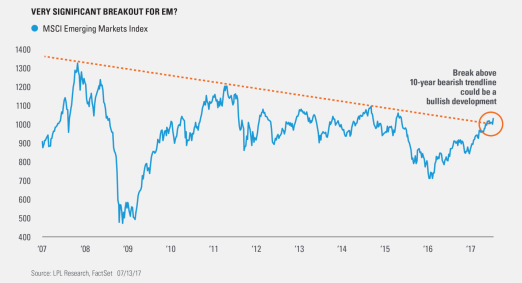

As a general note, emerging markets have benefitted till date from the surprise that came along with a weakening US dollar at least comparatively as many speculated at the beginning of the year that the US dollar would be even stronger than what it is now in turn having negative reverberating effects on the EEM fund. What also came as a surprise was very strong corporate earnings and modest valuations. But investors want to know if this rally for emerging markets is still in its early innings or closer to the ninth. One major positive suggesting it's early in the game is that the MSCI EEM index is in the process of breaking out of a bearish trendline going back nearly 10 years as can be seen in the chart below. This suggests that a major change in the negative trend is taking place and emerging markets could proverbially put more points on the board. That, obviously, includes China as well which has seen a much better July than previously anticipated.

While attempting to sort out all signals from the noise, it is difficult to believe that we are headed for years of high positive gains for emerging markets, not because of anything inherently wrong with emerging markets, but rather because of the way in which developed economies, particularly the United States, may bring down the rest of the world again like in 2008. Now this is not a prediction that the sky is going to fall tomorrow but it is important to be cautious when US markets are reaching highs consistently for months on end. In reality, too many strange signs are occurring in the market for this analysts' view and to determine that we are not due for some significantly turbulent waters ahead. One specific event underlines extreme weaknesses in the Trump trade which is that of healthcare reform in the Senate being now looking very unlikely to pass.

This was signaled earlier this week when Senate Majority Leader Mitch McConnel decided to pull the most recent iteration of repealing and replacing Obamacare. While this may seem unrelated, reasoning behind Trump trade was the anticipation of tax cuts. Without Congress being able to cut subsidies in Obamacare, these tax cuts cannot be passed with the so-called budgetary reconciliation that Republicans were hoping to pass it through with. Budgetary reconciliation basically means that if the bill doesn't add to the deficit, then they only need a simple majority or 51 senators to pass the bill. Without this, they need 2/3rds. Budgetary reconciliation for tax cuts is not achievable without cutting almost $1 trillion from healthcare subsidies and it does not seem likely that Republicans, with a slim majority in the Senate, will be able to convince Democrats to join them in tax cuts for millionaires and billionaires. Because of this, the Trump trade is, not entirely, but very closely approaching its death.

This may seem insignificant but US equity markets rose by almost 15% since Trump's ascendency into power. When will investors wake up and realize this trade is over? Some are trying to rationalize that the current valuation of US markets as a whole is justified now by strong company plans, strong earnings and basically strong essentials. This would be funny if the ramifications of such an already inflated market were not so dire. It is because of this that emerging markets and really the world as a whole is in high danger of at the very least a market correction if Trump and the Republicans cannot figure out how to pass some sort of Obamacare subsidiary reduction. Again though, these chances are small.

Perhaps investors will continue to put their head in the sand regarding the ballooning of US equities without a real convincing justification of its pricing. China, as the world's second largest economy with huge ties to US markets, is most at risk of this problem. Remember, people were talking about how inflating the market was before the Trump trade. Let's not lie to ourselves that some money in equity markets can still be made. Perhaps they will balloon even more. But let's also not lie to ourselves that a day of reckoning will eventually come which is especially important for Chinese equities given the volatility already inherent in their fluctuations.

--- END ---