Implementation of Scope Expansion of Deferred Withholding Tax Policy

on Distributed Profits Reinvested

by Foreign Investors for Direct Investment

分布式利润再投资延期预扣税政策扩大实施范围

分布式利润再投资延期预扣税政策扩大实施范围

财政部,国家税务总局,国家发展和改革委员会,商务部联合发布财税(2018)第102号“关于扩大暂行政策适用范围的通知” 不对海外投资者直接投资所使用的分布式利润征收预扣税(“102号通知”)以取代之前的财税(2017)第88号,关于暂不对分布式利润征收预扣税的政策问题的通知 (“第88号通知”)。

根据更新的102号通知,53号公告还扩大了外国投资者对再投资利润分配的税收延期政策的适用范围。 公告53自2018年1月1日起生效,而公告3自2018年1月1日起失效。

公告53作为102号文的实施指南和补充说明。进一步明确了合格再投资的若干条件,从而进一步扩大了税收延期政策的适用范围。 建议外国投资者积极考虑直接再投资的税收优惠政策的资格,并遵守税收优惠政策的实施规定。

The Ministry of Finance, the State Administration of Taxation (“SAT”), the National Development and Reform Committee and the Ministry of Commerce have jointly released Cai Shui (2018) No. 102, Circular on Expanding the Applicable Scope of the Policy of Temporarily Not Levying the Withholding Tax on Distributed Profits Used by Overseas Investors for Direct Investment (“Circular 102”) to replace the previous Cai Shui (2017) No. 88, Circular on Policy Issues concerning Temporarily Not Levying the Withholding Tax on Distributed Profits Used by Overseas Investors for Direct Investments (“Circular 88”).

The Ministry of Finance, the State Administration of Taxation (“SAT”), the National Development and Reform Committee and the Ministry of Commerce have jointly released Cai Shui (2018) No. 102, Circular on Expanding the Applicable Scope of the Policy of Temporarily Not Levying the Withholding Tax on Distributed Profits Used by Overseas Investors for Direct Investment (“Circular 102”) to replace the previous Cai Shui (2017) No. 88, Circular on Policy Issues concerning Temporarily Not Levying the Withholding Tax on Distributed Profits Used by Overseas Investors for Direct Investments (“Circular 88”).

In order to update the relevant implementation regulations, the SAT has published the Announcement of the SAT (2018) No. 53, Announcement of the SAT on Issues Concerning Expanding the Applicable Scope of the Policy of Temporarily Not Levying Withholding Tax on Distributed Profits Used by Overseas Investors for Direct Investments (“Announcement 53”) to replace the announcement on the Implementation of the Policy of Temporarily Not Levying the Withholding Tax on Distributed Profits Reinvested by Foreign Investors for Direct Investment (“Announcement 3”).

In response to the updated Circular 102, Announcement 53 has also expanded the application scope of the tax deferral policy on the reinvested profit distribution by foreign investors. Announcement 53 shall be effective from January 1, 2018, while Announcement 3 becomes ineffective from January 1, 2018.

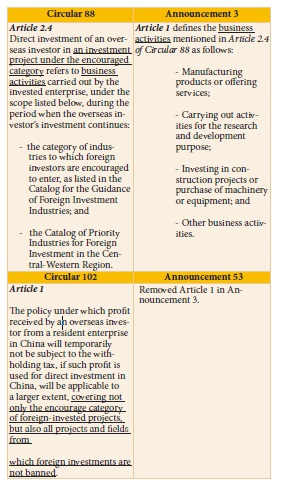

1. Expand Scope of Reinvestment

Announcement 53 has deleted the required business operation scope of the qualified investment under the encouraged category.

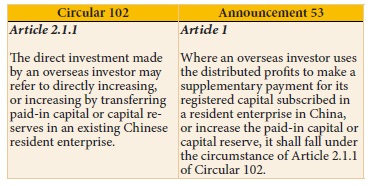

2. Qualified Scenario as Capital Increase

2. Qualified Scenario as Capital Increase

Announcement 53 has specified a scenario as qualified capital increase.

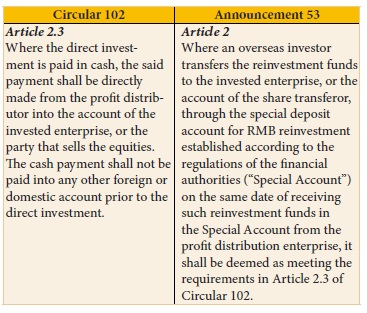

3. Qualified Scenario as Direct Payment

3. Qualified Scenario as Direct Payment

Announcement 53 has specified a scenario as qualified direct payment.

4. Effective Period

4. Effective Period

Announcement 53 is effective from January 1, 2018. For the distributed profits received from January 1, 2017 to December 31, 2017, Circular 88 and Announcement 3 still prevail and the tax incentives are only applicable to the projects under the encouraged category.

Conclusion

Announcement 53 serves as the implementation guidance and supplementary explanation of Circular 102. It has further clarified certain conditions of qualified reinvestment, and in consequence further expands the application scope of the tax deferral policy. Foreign investors are suggested to actively consider the eligibility for the tax preferential policy for direct reinvestment, and conform to the implementation regulations in the application of the tax incentives. At the same time, the investors need to keep a close contact with the in-charge tax authority to obtain a better understanding of the local practice of unclarified issues, such as the treatment of refunded tax from the reinvestment of dividend distribution.