Individual Income Tax Rules

Changes Relevant to Foreign Individuals

By Edmund Yang, Tax Partner, PricewaterhouseCoopers Beijing

个人所得税规则

个人所得税规则

与外国人有关的变化

新的中国个人所得税(“IIT”)法及其实施规则的颁布标志着向新的个人所得税制度的转变。对在中国工作的外国人来说,了解一些变化和要求对他们来说很重要。

一个主要的根本变化是中国税务居民的定义。根据新的个人所得税法,在中国没有固定住所的个人在中国居住183天后,被视为中国税务居民。新的“6年”规则也采用了中国税务居民的这一新定义。

此外,根据新的“6年”规定,非中国居住的个人在全球收入中不会受到IIT的限制,前提是他们连续六年没有在中国居住183天或更长时间,而且他们已经完成了所需的记录备案。关于延长五年至六年的问题,中国国家税务总局(“SAT”)需要进一步澄清如何完成备案要求以及如何对2019年之前的一年进行分类累积的问题。

The promulgation of the new PRC Individual Income Tax (‘IIT’) Law and its implementation rules signifies a shift towards a new IIT regime. To foreign individuals working in China, it is important for them to understand some of the changes and requirements.

The promulgation of the new PRC Individual Income Tax (‘IIT’) Law and its implementation rules signifies a shift towards a new IIT regime. To foreign individuals working in China, it is important for them to understand some of the changes and requirements.

One major fundamental change is the definition of a China tax resident. Under the new IIT Law, individuals without domicile in China are considered China tax residents once they have resided 183 days in China during the calendar year concerned. This new definition of China tax resident is also adopted for the new ‘6-year’ rule. Unlike the old ‘5-year’ rule requiring non-China domiciled individuals to spend more than 30 consecutive days, or 90 days in total, outside China to restart the 5-year count, non-China domiciled individuals can now restart the 6-year count by spending more than 30 consecutive days outside China during a calendar year, before reaching the 6-year threshold.

Moreover, under the new ‘6-year’ rule, non-China domiciled individuals would not be subject to IIT on their worldwide income providing they have not resided 183 days or more in China for six consecutive years, plus they have completed the required record filing with the in-charge tax bureau. In connection with the extension from five years to six years, further clarification from the PRC State Administration of Taxation (‘SAT’) is required on questions such as how to complete the record filing requirement, and how to classify a year prior to 2019 with accumulated absence of 90 days under the old ‘5-year’ rule.

Besides being a China tax resident may impact a non-China domiciled individual’s IIT liability on his or her worldwide income, there are other implications as well. For those who are China tax residents, their employers should use the following new accumulated method for calculating the monthly IIT withholding amount.

Besides being a China tax resident may impact a non-China domiciled individual’s IIT liability on his or her worldwide income, there are other implications as well. For those who are China tax residents, their employers should use the following new accumulated method for calculating the monthly IIT withholding amount.

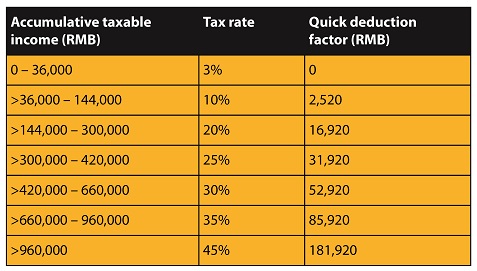

Monthly IIT withholding amount = (Accumulative taxable amount* x Withholding tax rate – Quick deduction factor) – Accumulative tax credit – Accumulative tax withheld

*Accumulative taxable amount = Accumulative income – Accumulative tax exempted income – Accumulative standard basic deduction – Accumulative specific deductions – Accumulative specific additional deductions – Accumulative other deductions

Specific deductions refer to statutory social security and housing fund contributions, whereas other deductions include deductible items provided by various IIT regulations, such as commercial health insurance eligible for IIT incentive, employee contributions to corporate annuity, and commercial endowment insurance eligible for IIT deferral treatment, etc…

Under the new IIT Law, standard basic deduction has been increased to RMB60,000 per year (i.e., RMB5,000 per month). In addition, employment income is now grouped under comprehensive income together with remuneration for labor services, manuscripts and royalty income, subject to the IIT rates table below.

With the introduction of the new accumulated method, individuals may need to manage their cash flow for minimizing the financial impact from the increasing amount of monthly tax withheld. However, this new method is not applicable to non-residents (non-China domiciled individuals who have not resided 183 days or more in China during the tax year concerned). The IIT withholding of non-residents’ income should be calculated by types and by items on a monthly or transaction basis, in accordance with the new IIT Law and using the monthly tax rates table applicable to comprehensive income.

With the introduction of the new accumulated method, individuals may need to manage their cash flow for minimizing the financial impact from the increasing amount of monthly tax withheld. However, this new method is not applicable to non-residents (non-China domiciled individuals who have not resided 183 days or more in China during the tax year concerned). The IIT withholding of non-residents’ income should be calculated by types and by items on a monthly or transaction basis, in accordance with the new IIT Law and using the monthly tax rates table applicable to comprehensive income.

For those foreign nationals who have been enjoying the non-taxable benefits (i.e., child education, housing, language training, home leave, relocation, meals and laundry) provided by the preferential tax policy, they can continue to enjoy these non-taxable benefits for 3 more years during the transition period of 2019 to 2021.

Alternatively, foreign nationals who qualify as residents may choose to claim the specific additional deductions (i.e., child education, continuing education, major medical expense, mortgage interest, rental expense and elderly care) instead of the non-taxable benefits. This selection between non-taxable benefits and specific additional deductions cannot be changed during the same tax year.

Furthermore, foreign nationals, who qualify as residents, can enjoy the preferential tax treatments applicable to annual bonus and employee equity incentive plan income from listed companies during the transition period of 2019-2021. For those who cannot enjoy the preferential tax treatments, these two income items should be taxed together with the other monthly employment income.

Furthermore, foreign nationals, who qualify as residents, can enjoy the preferential tax treatments applicable to annual bonus and employee equity incentive plan income from listed companies during the transition period of 2019-2021. For those who cannot enjoy the preferential tax treatments, these two income items should be taxed together with the other monthly employment income.

According to the new IIT Law and implementation rules, annual reconciliation filing should be completed between March 1st and June 30th of the following year for the following situations:

• individual with comprehensive income from more than one source and the annual taxable amount exceeds RMB60,000

• individual with other comprehensive income, besides employment income, and the annual taxable amount exceeds RMB60,000

• individual with tax payable for the tax year below the amount of tax withheld

• individual applying for tax refund (e.g., tax refund due to claim of major medical expense addition deduction).

In addition to annual reconciliation filing, individual tax filing is required for the following situations as well:

• Individual with business operation income (annual filing due date is March 31st of the subsequent year)

• Individual with taxable income to which the tax withholding agent has not withheld the IIT payable (annual filing due date is March 1st and June 30th of the subsequent year)

• Individual with overseas income (annual filing due date is March 1st and June 30th of the subsequent year)

• Tax filing for cancelation of China household registration for individual who has immigrated overseas (before cancelation of China household registration)

• Non-resident with employment income from more than one source within China (monthly filing due date is 15th of the subsequent month, annual filing due date is June 30th of the subsequent year, or before departure from China, whichever is earlier).

Henceforth, individual who only has taxable employment income and the IIT payable thereon has been fully settled through his/her employer’s monthly tax withholdings are not required to perform the annual reconciliation filing.

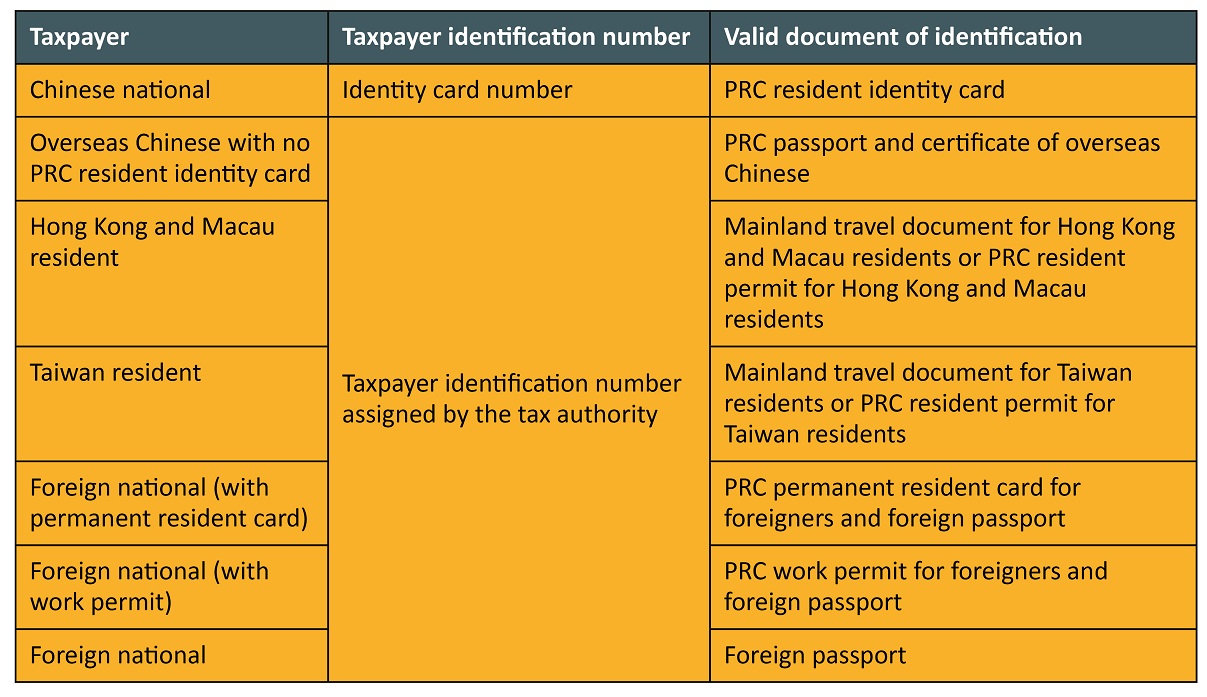

Another important point is each individual taxpayer has one unique taxpayer identification number for handling all his/her tax related matters. The following table sets out the taxpayer identification number for different types of individual taxpayers.

To properly assess the IIT implications and filing obligation, as well as optimal utilization of the available deductions and preferential treatments, taxpayers and their withholding agents need to have a good understanding of the new IIT Law and its implementation rules. For example, the differences in withholding and filing requirements, plus tax treatments, applicable to non-China domiciled individuals who are China tax residents versus those who are non-China tax residents.

To properly assess the IIT implications and filing obligation, as well as optimal utilization of the available deductions and preferential treatments, taxpayers and their withholding agents need to have a good understanding of the new IIT Law and its implementation rules. For example, the differences in withholding and filing requirements, plus tax treatments, applicable to non-China domiciled individuals who are China tax residents versus those who are non-China tax residents.

While the introduction of unique taxpayer identification number is an enhancement to the tax authority’s administration and enforcement abilities, it also may increase the risk exposure of non-tax compliance.

Although the documents released by the SAT so far have provided details to the implementation of the new IIT Law and its implementation rules, there are still uncertainties which require further clarification from the SAT. For those who have questions on the new changes, it would be advisable to do some research, and/or seek guidance from tax professional.