.png) Background

BackgroundUnder the Chinese legal framework, foreign exchange control is very famous in the sense that almost any in-flow or out-flow of foreign exchange across the border is strictly regulated. With regards to trade in goods, the foreign exchange verification system has been implemented for around 20 years, according to which, for each exportation and importation, verification by the foreign exchange administration is necessary, triggering time-consuming and complicated formalities for exporters and importers.

Considering that the scale of trade in goods in China has developed rapidly and tremendously and in order to simplify the procedures to facilitate the foreign trade under the current international economic situation, the State Administration of Foreign Exchange (SAFE) of China considers it to be a good time to implement reforms for the current foreign exchange system for trade in goods, though there have been some pilot reforms. Accordingly, on 27 June, 2012, the SAFE issued the Notice Concerning Relevant Issues on Circulating Several Regulations Regarding Foreign Exchange Administration of Trade in Goods (Huifa[2012]No.38), which is effective as of 1 August, 2012, under which, Guidelines for Foreign Exchange Administration for Trade in Goods, its implementing rules, as well as operational rules and the other two relevant rules, are promulgated (Reform Regulations), replacing all of the former regulations and rules regarding the foreign exchange administration for trade in goods.

Evolution of the Reform

As mentioned above, actually the content of the Reform Regulations are not entirely new, and are based on several pilot reforms introduced by SAFE through step-by-step reform since 2010.

.png)

In May 2010, SAFE had a pilot reform regarding the importation of goods among 5 provinces and 2 municipalities, including Tianjin, Qingdao, Fujian province, Jiangsu province, Shandong province, Hubei province and Inner Mongolia Autonomous Region. Since October 2010, exporters in 3 provinces and 1 municipality, including Guangdong province, Jiangsu province, Shandong province and Beijing, were allowed by SAFE to deposit their foreign exchange incomes arising from exportation of goods into their overseas accounts subject to certain conditions. In December 2010, the aforementioned pilot reforms have been extended all across the nation and the foreign exchange control system for the importation of goods and overseas deposit of exportation incomes came into shape.

In December 2011, SAFE launched a pilot reform involving trade in goods (from the view of both importation and exportation of goods) amongst 5 provinces and 2 municipalities, including Jiangsu province, Shandong province, Hubei province, Zhejiang province (excluding Ningbo city), Fujian province (excluding Xiamen city), Dalian and Qingdao. After an approximately 6-month pilot reform, SAFE extends the pilot reform to the whole nation and thus comes the reform which consolidates all of the previous polite reforms and also improves the administration system. Following the reforms, the foreign exchange administration system for trade in goods has the following main key features:

Key Features

● Category of Enterprise

Enterprises engaging in the foreign trade activities (either importation or exportation) would be graded by SAFE into Category A, B and C,, taking into consideration the off-site and on-site inspection results by SAFE and compliance situation of the enterprises. The list of enterprises in different categories will be published by SAFE and available to the general public when SAFE deems it necessary. The formalities and requirements imposed on the enterprises, as well as the supervision and control from SAFE varies depending on the categories to which the enterprise belongs, which are illustrated as follows:

1) Category A

• Simplified procedures:

An enterprise falling into Category A could directly perform or receive payment by presenting any of the customs reports, contract or invoice before the relevant banks;

• Special report of trade financing:

For the advance collection/payment in the term of over 30 days, import trade financing with over 90-day usage letter of financing or an import bill advanced by overseas institutions, and the deferred collection/payment in the term of over 90 days, the enterprise shall report to the competent local counterpart of SAFE through the online system within 30 days after actual occurrence of the above trade financing.

2) Category B

• Quota administration:

Based on the performance, as well as actual foreign trade situation of the enterprise of Category B, SAFE will verify a foreign exchange payable/receivable quota for the enterprise of Category B (quota). Within the quota, the enterprise may perform or receive payment by presenting the custom report, contract and invoice before the relevant banks; for transactions beyond the quota, the foreign exchange payment and collection are subject to the prior-registration of the competent SAFE.

• Special report of trade financing:

For any advance collection/payment, import trade financing with over 90-day usage letter of financing or import bill advancements by overseas institutions, and the deferred collection/payment in the term of over 30 days, the enterprise shall report to the competent local SAFE through the online system within 30 days after actual occurrence.

• Main limitations:

Certain transactions (such as intermediary trade with over 90-day trade financing, import with over 90-day deferred payment, and export with over 90-day deferred or advance collection, etc) are not allowed, collections cannot be deposited in the overseas account.

3) Category C

• Case-by-case registration:

The registration before the competent local SAFE with respect to the collections and payments of foreign exchange has to be conducted on a case-by-case basis;

• Special report of trade financing:

The report obligations regarding trade financing for the enterprise of Category C are the same as enterprise of Category B; moreover, for each advanced payment above USD 50,000 under importation of goods, bank guarantee for the advance payment shall be provided by overseas contracting parties;

• Main limitations:

Certain transactions (such as any intermediary trade, import trade financing with over 90-day usage letter of financing or import bill advance by overseas institutions, import with over 90-day deferred payment and export with over 90-day deferred or advance collection, etc.) are not allowed, and the overseas account (if existing) shall be closed.

In terms of the above, it could be concluded that enterprises of Category A are entitled to follow more simplified procedures and enjoy considerable autonomy in their foreign trade activities. Generally speaking, enterprises which comply with the rules and regulations of SAFE could be categorised as A. On the other hand, enterprises which have violations may be categorised as B or C depending on different situations and thus would be subject to more strict supervision by SAFE. The supervision term for each category usually lasts for one year, upon the expiry of which SAFE would assess the compliance performance of enterprises and may adjust the categorisation.

● Streamlined process for export customs declaration and tax rebate

Before 1 August, 2012, other than the exporters in the pilot areas as mentioned above, in order to apply for a tax rebate, exporters shall apply for the verification form for collection of foreign exchange under exportation before competent local SAFE. Upon the effectiveness of the Reform Regulations, the paper verification form has been abolished and will not be required for export customs declaration and tax rebate.

● Report Obligation and Inspection System

Per each foreign exchange payment or collection, enterprises could report to relevant banks through an online system or written report form. Within 5 working days after payment or collection, banks shall declare the transactions to the competent local SAFE through online system.

Based on the information reported by enterprises and banks, SAFE will monitor the total volume of capital flow against the goods flow on a macro basis. By setting various targets (such as the difference between goods flow and capital flow, the proportion of trade financing etc), the competent local SAFE would assess the performance of enterprises on a monthly basis. In the event of unusual circumstances (such as over-abound trade financing, refund of over USD 500,000) detected through the online system, an off-site or on-site inspection could be triggered and certain supporting documents and explanations should be provided by the enterprise inspected.

According to the result of off-site and on-site inspection, competent local SAFE may at any time adjust the categorisation of the enterprises. Enterprises of Category A may be downgraded to Category B or C if certain violations of the foreign exchange administration rules are constituted. On the contrary, if an enterprise of Category B or C has been complying with the foreign exchange administration rules during the one-year supervision term, they may be upgraded to Category A after the assessment by the competent local SAFE upon expiry of the supervision term.

Our Observations

It is foreseeable that the Reform Regulations will facilitate international trade and simplifies the procedure and process of trade in goods. Consequently, from the view of formalities, the transaction cost could be reduced and the operational efficiency could be achieved.

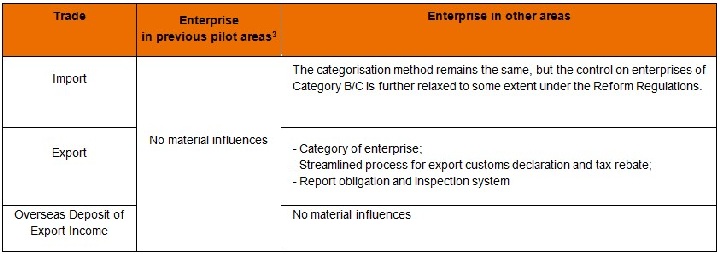

In line with the implementation of the Reform Regulations, a new mechanism for monitoring foreign exchange collection/payment under trade in goods is established in China. Considering the previous pilot reforms launched by SAFE, influences of the Reform Regulations on the existing enterprises may vary, which could be referred to the following chart:

Nevertheless, it shall be noticed that, being efficient does not mean that such administration will become relaxing and loosened. The classification of the enterprises will ensure that SAFE focuses more on high-risk enterprises and the information sharing system among SAFE, General Administration Committee and State Administration for Taxation will further strengthen the cooperation amongst different authorities involved in trade in goods and form a regulatory resultant force towards the foreign trade enterprises.

In conclusion, as a general suggestion, the enterprises engaging in foreign trade in China should respect and comply with the foreign exchange regulations in order to maintain the good performance and favourable category. As for the foreign business operators who are doing trading related business with Chinese exporters and importers, it would be better to check the category of their business partners in China so as to know whether certain trade financing arrangements are feasible according to the Reform Regulations.

.png)